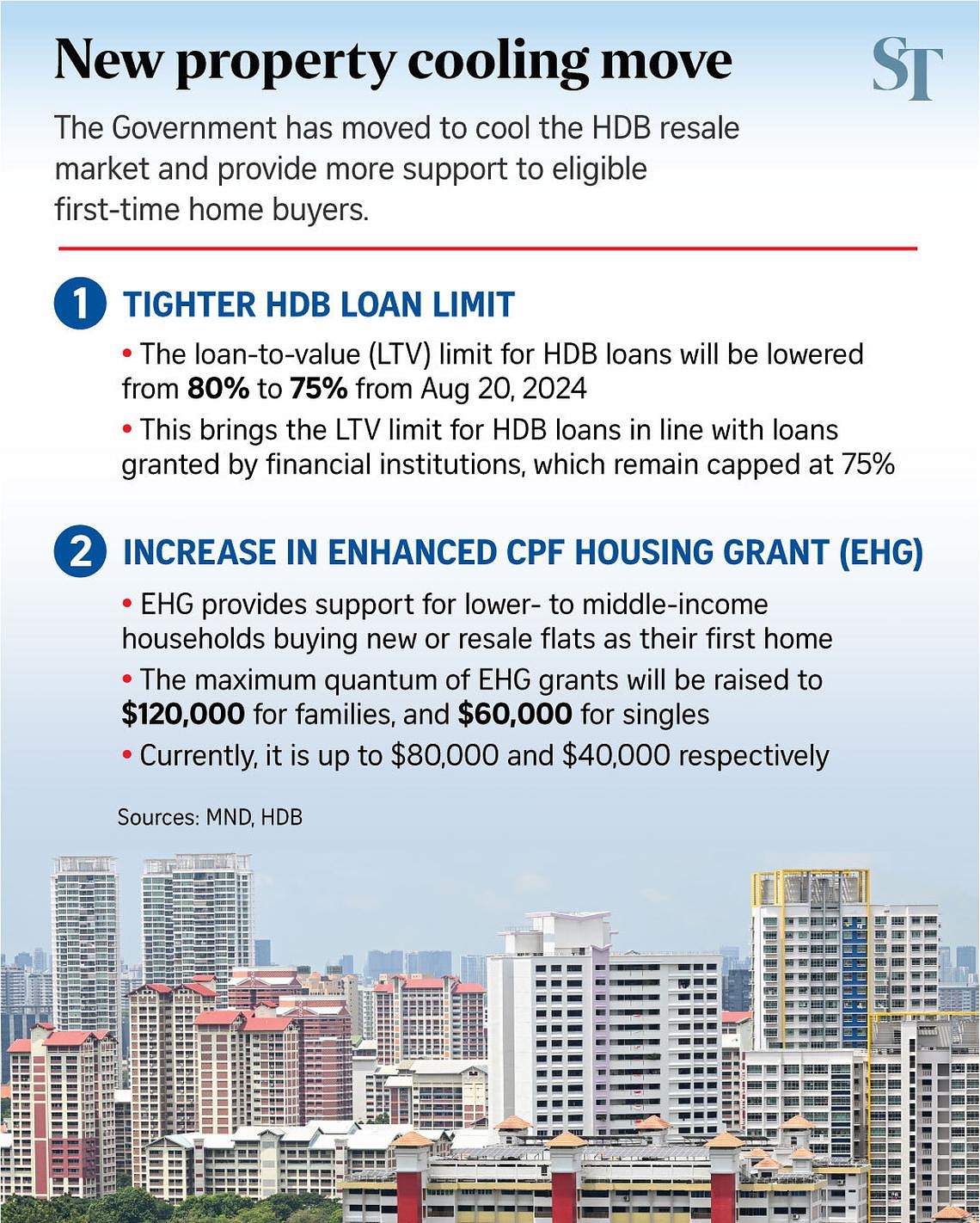

SINGAPORE - The loan-to-value limit for HDB loans has been lowered from 80 per cent to 75 per cent as part of a move introduced on Aug 20 to cool the resale flat market.

The Straits Times answers some questions about the latest cooling measure.

1. What is the loan-to-value limit?

The loan-to-value (LTV) limit is the maximum amount one can borrow from the HDB to fund a new or resale flat purchase.

This is the third time the LTV limit has been lowered. It was previously tightened from 90 per cent to 85 per cent in December 2021, and then reduced to 80 per cent in September 2022.

From Aug 20, it has been brought down to 75 per cent in an effort to further stabilise the HDB resale market and encourage flat buyers to borrow prudently, the authorities said.

The LTV limit for bank loans remains unchanged at 75 per cent.

2. Who will be affected by the tightened LTV limit, and when will it kick in?

Flat buyers who have submitted the complete resale application to HDB – both the buyers’ and sellers’ portions – from Aug 20 will be subject to the lower LTV limit of 75 per cent.

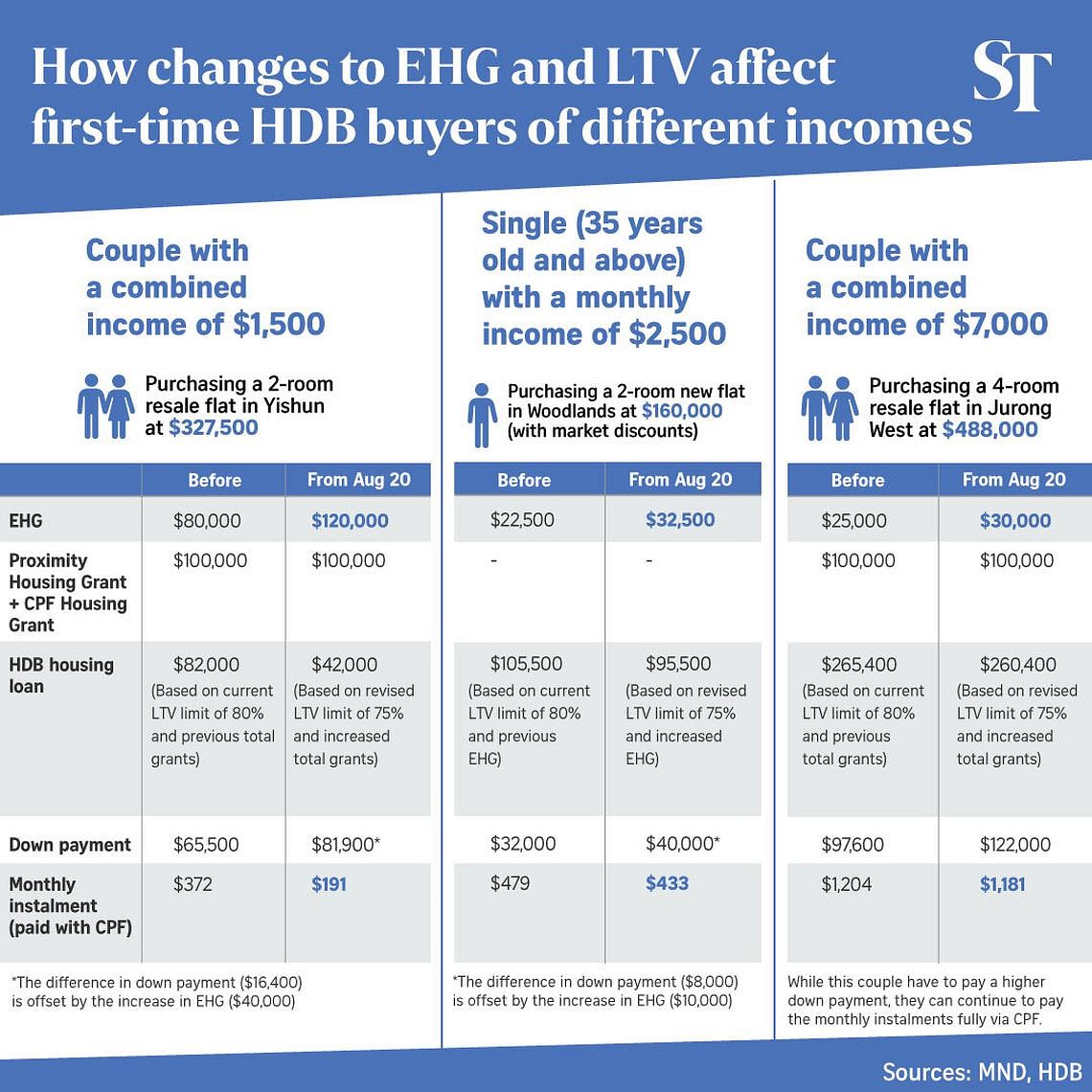

This means buyers will have to fork out a down payment of 25 per cent of the flat’s purchase price in cash or Central Provident Fund (CPF) savings.

For example, a buyer who wants to purchase a $500,000 flat can get only a $375,000 loan, down from $400,000 before. He would have to top up $25,000 more in cash or CPF.

To qualify for an HDB loan, buyers are subject to an income ceiling, currently pegged at $14,000 a month, among other conditions.

3. Will successful applicants in the June and earlier Build-To-Order (BTO) launches be affected by the new measure?

No, the LTV limit for HDB housing loans will remain at 80 per cent for successful applicants in those launches.

For prospective BTO applicants, the new measure will take effect from the October sales exercise, which will offer about 8,500 flats across Ang Mo Kio, Bedok, Bukit Batok, Geylang, Jurong West, Kallang/Whampoa, Pasir Ris, Sengkang and Woodlands.

4. Will resale buyers who have paid their option fee or exercised their option to purchase, but did not submit the HDB resale application before Aug 20, be subjected to the lower LTV limit?

Yes, they will be subjected to the lower LTV limit of 75 per cent.

National Development Minister Desmond Lee said in a media briefing on Aug 20 that those who are concerned about the impact of the tightened LTV on their housing arrangements may approach HDB for assistance if they have extenuating circumstances. It will be assessed on a case-by-case basis.

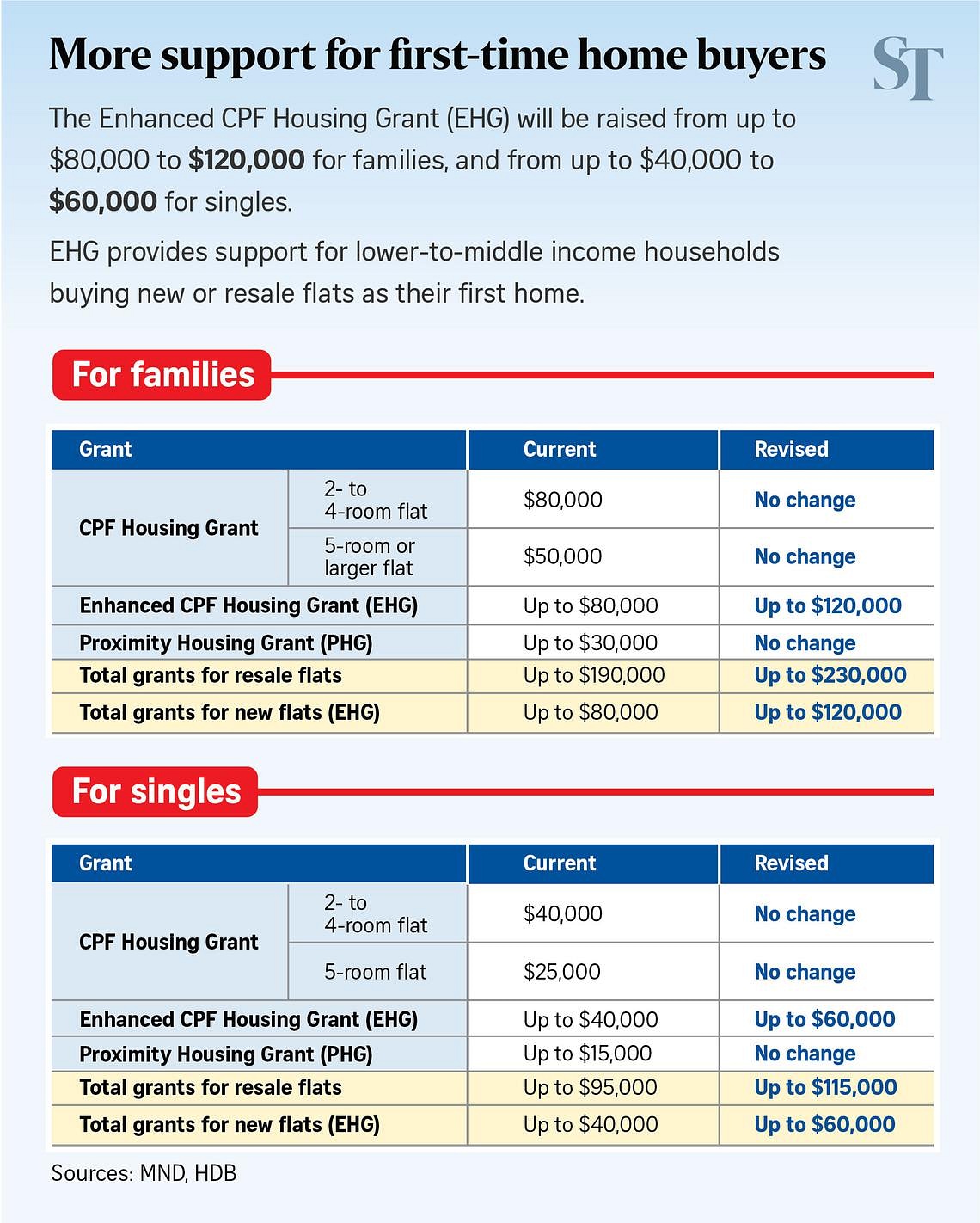

5. Who will benefit from the increased Enhanced CPF Housing Grant?

First-time home buyers will be able to tap more financial support under the Enhanced CPF Housing Grant (EHG).

The maximum grant amount will be raised from $80,000 to $120,000 for families, and from $40,000 to $60,000 for singles.

Depending on monthly household income, the increase will range from $5,000 to $40,000 for families and from $2,500 to $20,000 for singles.

Lower-income households will receive the most support.

Families with an average monthly household income of $1,500 and below can tap the full $120,000 grant, while singles with a monthly income of $750 and below will get the full $60,000 in financial support.

There will be no change in grant amount for families with an average monthly household income of $8,001 to $9,000, and singles with a monthly income of $4,001 to $4,500.

6. When would buyers be able to tap the increased EHG?

Prospective BTO applicants who have or are intending to apply for an HDB Flat Eligibility (HFE) letter can tap the revised EHG from the October sales exercise.

HDB will update applicants’ HFE letter to reflect the new grant amount, and will notify them by e-mail.

The revised EHG will not apply retrospectively for flats that have already been launched.

For resale buyers, eligible first-timers who have not yet completed their resale transaction will receive the increased grant.

The amount will be credited into their CPF accounts within two months from the date of completion of their resale transaction.

7. What were the previous cooling measures?

This is the fourth round of measures since December 2021.

The previous round of measures in April 2023 raised additional buyer’s stamp duty (ABSD) rates for Singaporeans and permanent residents buying their second and subsequent properties. The rate for foreigners buying any residential property was also doubled from 30 per cent to 60 per cent.

The hikes were aimed at preventing property prices from being pushed up by investors, and prioritising Singaporeans buying homes for owner-occupation.

Prior to this move, ABSD rates for home buyers and developers were raised in December 2021.

In September 2022, a 15-month wait-out period was introduced for private home owners who wish to buy a resale flat, in a move to moderate demand in the HDB resale market.

Higher floor rates for the total debt servicing ratio and mortgage servicing ratio for property loans granted by private financial institutions and the HDB were also introduced to address the issue of overborrowing.